ジボット=アンドリュース検定(Zivot Andrews test) により 構造変化を考慮した 単位根検定を行います。

以降の数式、導出は https://www.fbc.keio.ac.jp/~tyabu/keiryo/perron.pdf を引用参照しています。

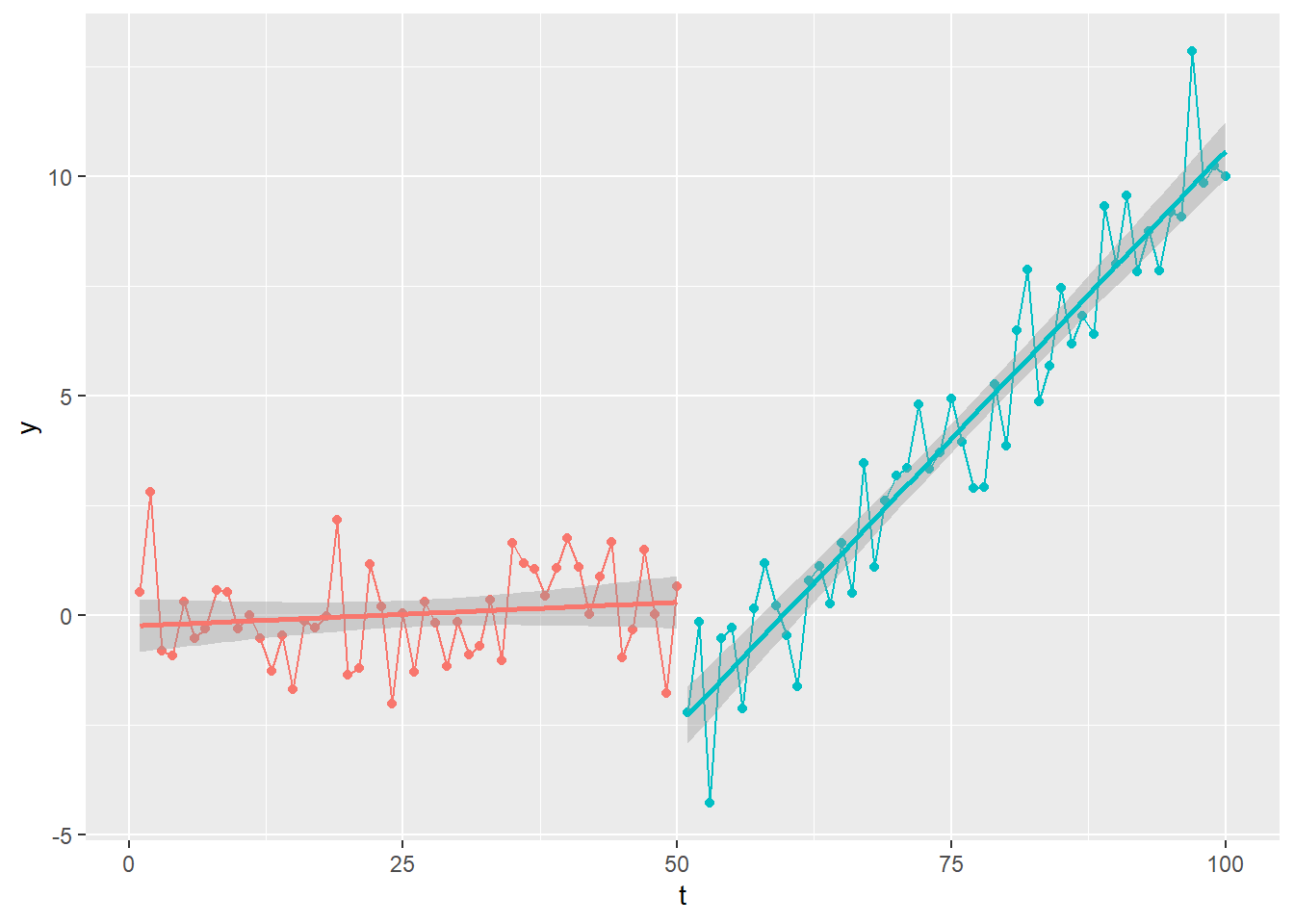

それでは R で 構造変化を考慮した単位根検定 を行います。

なお、以降有意水準は 5% とします。また、ラグは共通して lag = 3 としていますが本件の場合は数値自体に意味はありません。

始めにサンプルデータ y を作成します。

ベースとするサンプルは 100個(n) の ホワイトノイズ。t が 50(bp) 以降、切片(intercept) を -2、傾き(slope) を 0.25 とした 構造変化 を加えます。

seed <- 20240821

set.seed(seed)

library(dplyr)

library(ggplot2)

n <- 100

t <- seq(n)

bp <- 50

intercept <- -2

slope <- 0.25

y <- rnorm(n) + (intercept + (t - bp) * slope) * (seq(n) > bp)

ggplot(mapping = aes(x = t, y = y, colour = seq(n) > bp)) +

geom_line() +

geom_point() +

geom_smooth(method = "lm") +

theme(legend.position = "none")

構造変化を考慮しないADF検定 を掛けますと、ベースは ホワイトノイズ ですが 単位根 は棄却されません。

lag <- 3

urca::ur.df(y = y, type = "trend", lags = lag) %>% urca::summary()

###############################################

# Augmented Dickey-Fuller Test Unit Root Test #

###############################################

Test regression trend

Call:

lm(formula = z.diff ~ z.lag.1 + 1 + tt + z.diff.lag)

Residuals:

Min 1Q Median 3Q Max

-3.8809 -0.7900 0.1036 0.7850 3.6112

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.443714 0.336357 -1.319 0.190458

z.lag.1 -0.060284 0.067779 -0.889 0.376146

tt 0.016224 0.007929 2.046 0.043664 *

z.diff.lag1 -0.788531 0.116211 -6.785 1.19e-09 ***

z.diff.lag2 -0.507054 0.125915 -4.027 0.000118 ***

z.diff.lag3 -0.201115 0.105328 -1.909 0.059394 .

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.25 on 90 degrees of freedom

Multiple R-squared: 0.4367, Adjusted R-squared: 0.4054

F-statistic: 13.95 on 5 and 90 DF, p-value: 4.338e-10

Value of test-statistic is: -0.8894 3.1978 2.8176

Critical values for test statistics:

1pct 5pct 10pct

tau3 -4.04 -3.45 -3.15

phi2 6.50 4.88 4.16

phi3 8.73 6.49 5.47そこで、構造変化を考慮した単位根検定 として ジボット=アンドリュース検定(Zivot Andrews test) を利用します。

ジボット=アンドリュース検定(Zivot Andrews test) の流れは次の通りです。

- 標本期間の初めから及び最後から15%のデータを構造変化点候補から除きます。

- 構造変化点候補全てについて ペロン検定 により t検定統計量 \(\tau\left(T_B\right)\) を求めます。

- 求めた t検定統計量 \(\tau\left(T_B\right)\) のうち、最小の検定統計量 \(\textrm{inf-}t\) を臨界値と比較します。

それでは始めに構造変化点候補の下限 \(T_{min}\) と上限 \(T_{max}\) を求めます。

T_min <- n * 0.15

T_max <- n * (1 - 0.15)

list(T_min = T_min, T_max = T_max)$T_min

[1] 15

$T_max

[1] 85よって、構造変化点候補は \(T_B=(15,16,17,\cdots,83,84,85)\) となります。

続いて ペロン検定 により構造変化点候補毎の検定統計量を求めます。

次の ドリフト項、トレンド項 いずれも あり のモデルを考えます。

\[y_t=a_0+\gamma t+\theta_0DU_t+\theta_1DT_t+a_1y_{t-1}+u_t\] 同モデルに対して \[\textrm{H}_0:a_1=1,\,\textrm{H}_1:a_1<1\] とする検定が ペロン検定 です。

構造変化点を bp = 50 とした例を以下に示します。

fun_Perron_test <- function(y, bp) {

sample.df <- y %>% data.frame()

sample.df[, 2] <- head(y, -1) %>% c(NA, .)

sample.df[, 3] <- seq(y)

y.diff <- y %>%

diff(lag = 1, differences = 1) %>%

head(n - 2)

sample.df <- cbind(sample.df, embed(x = y.diff, dimension = lag) %>% rbind(matrix(nrow = lag + 1, ncol = lag), .))

sample.df$DU <- c(rep(0, bp), rep(1, n - bp))

sample.df$DT <- c(rep(0, bp), seq(n - bp))

sample.df <- sample.df %>% na.omit()

colnames(sample.df) <- c("y_t", "y_{t-1}", "t", seq(lag) %>% paste0("Δy_{t-", ., "}"), "DU", "DT")

result.lm <- lm(sample.df) %>% summary()

return(result.lm)

}

result.lm <- fun_Perron_test(y = y, bp = 50)

result.lm

Call:

lm(formula = sample.df)

Residuals:

Min 1Q Median 3Q Max

-2.5289 -0.7785 -0.0313 0.6663 3.0432

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.54972 0.38817 -1.416 0.160247

`y_{t-1}` -0.02723 0.19167 -0.142 0.887340

t 0.01999 0.01284 1.556 0.123206

`Δy_{t-1}` -0.08640 0.16781 -0.515 0.607934

`Δy_{t-2}` -0.11131 0.13342 -0.834 0.406394

`Δy_{t-3}` -0.05308 0.09651 -0.550 0.583734

DU -3.02674 0.75136 -4.028 0.000119 ***

DT 0.25078 0.04669 5.371 6.32e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.097 on 88 degrees of freedom

Multiple R-squared: 0.9146, Adjusted R-squared: 0.9078

F-statistic: 134.6 on 7 and 88 DF, p-value: < 2.2e-16\(\textrm{H}_0:a_1=1\) であるため、t検定統計量 は \[(推定値-1)/標準偏差\]として求めます。

(coef(result.lm)[2, 1] - 1) / coef(result.lm)[2, 2][1] -5.359321それでは構造変化点候補毎に ペロン検定 を掛けて、\(\textrm{inf-}t\) を求めます。

fun_Zivot_Andrews_test <- function(y, bp) {

if (T_min <= bp & bp <= T_max) {

result.lm <- fun_Perron_test(y = y, bp = bp)

((coef(result.lm)[2, 1] - 1) / coef(result.lm)[2, 2]) %>% return()

} else {

return(NA)

}

}

t <- sapply(X = seq(n), FUN = function(bp) fun_Zivot_Andrews_test(y = y, bp = bp))

min_T <- which.min(t)

inf_t <- t[min_T]

list(min_T = min_T, inf_t = inf_t)$min_T

[1] 50

$inf_t

[1] -5.359321\(\textrm{inf-}t\) は-5.3593207、構造変化点(bp) は50 となりました。

トレンド項あり、ドリフト項あり の場合の \(\textrm{inf-}t\) の 臨界値(Critical Value) を次の資料から引用します。

- Zivot, E., & Andrews, D. W. K. (1992). Further Evidence on the Great Crash, the Oil-Price Shock, and the Unit-Root Hypothesis. Journal of Business & Economic Statistics, 10(3), 251.

| 有意水準 | 臨界値 |

|---|---|

| 1.0% | -5.57 |

| 2.5% | -5.30 |

| 5.0% | -5.08 |

| 10.0% | -4.82 |

| 50.0% | -3.98 |

| 90.0% | -3.25 |

| 95.0% | -3.06 |

| 97.5% | -2.91 |

| 99.0% | -2.72 |

Model (A) permits an exogenous change in the level of the series, Model (B) allows an exogenous change in the rate of growth, and Model (C) admits both changes.

出典: Zivot, E., & Andrews, D. W. K. (1992). Further Evidence on the Great Crash, the Oil-Price Shock, and the Unit-Root Hypothesis. Journal of Business & Economic Statistics, 10(3), 251.

有意水準5% の場合の 臨界値 は -5.08 、\(\textrm{inf-}t\) は -5.359321 ですので、\(\textrm{H}_0:a_1=1\) は棄却されます。

なお、ur.za {urca} を利用して Zivot and Andrews Unit Root Test が行えます。上記 Rコードは 同関数を参考にしました。

urca::ur.za(y = y, model = "both", lag = lag) %>% urca::summary()

################################

# Zivot-Andrews Unit Root Test #

################################

Call:

lm(formula = testmat)

Residuals:

Min 1Q Median 3Q Max

-2.5289 -0.7785 -0.0313 0.6663 3.0432

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) -0.54972 0.38817 -1.416 0.160247

y.l1 -0.02723 0.19167 -0.142 0.887340

trend 0.01999 0.01284 1.556 0.123206

y.dl1 -0.08640 0.16781 -0.515 0.607934

y.dl2 -0.11131 0.13342 -0.834 0.406394

y.dl3 -0.05308 0.09651 -0.550 0.583734

du -3.02674 0.75136 -4.028 0.000119 ***

dt 0.25078 0.04669 5.371 6.32e-07 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 1.097 on 88 degrees of freedom

(4 observations deleted due to missingness)

Multiple R-squared: 0.9146, Adjusted R-squared: 0.9078

F-statistic: 134.6 on 7 and 88 DF, p-value: < 2.2e-16

Teststatistic: -5.3593

Critical values: 0.01= -5.57 0.05= -5.08 0.1= -4.82

Potential break point at position: 50 検定統計量(-5.3593 )、構造変化点(50) ともに一致しています。

以上です。